We audit a lot of P&Ls.

And right now, the “Software & Subscriptions” line item is out of control for most brands.

We are seeing Shopify stores doing $10M in revenue paying for 35+ different apps. It’s a “Franken-stack”, a mess of disconnected tools bleeding monthly recurring revenue (MRR) and creating a nightmare for the ops team.

How did we get here?

The Era of Unbundling (2019-2022) A few years ago, the philosophy was “best-in-class.” You wanted the #1 specific app for referrals, a different app for reviews, another for loyalty, and another for surveys. We unbundled the entire marketing stack into dozens of “point solutions.”

It worked when capital was cheap and growth was easy.

The Era of Consolidation (Now) In 2025, the pendulum has swung back. The “unbundling” created fractured data, bloated costs, and operational drag.

Now, we are seeing the “Great Re-Bundling.”

Smart operators are ruthlessly auditing their tech stacks. They are cutting the single-use tools and moving to unified platforms that handle multiple jobs. If an app only does one thing, it’s on the chopping block.

The 3-Step Audit If you haven’t looked at your app list in Q4, do this now:

- Export your App List: Highlight every app that costs >$300/mo.

- Check for Overlap: Do you have a loyalty app and a separate referral tool? Do you have a reviews app and a separate UGC collector?

- Consolidate: Look for platforms that can do 3-4 of these jobs in one place.

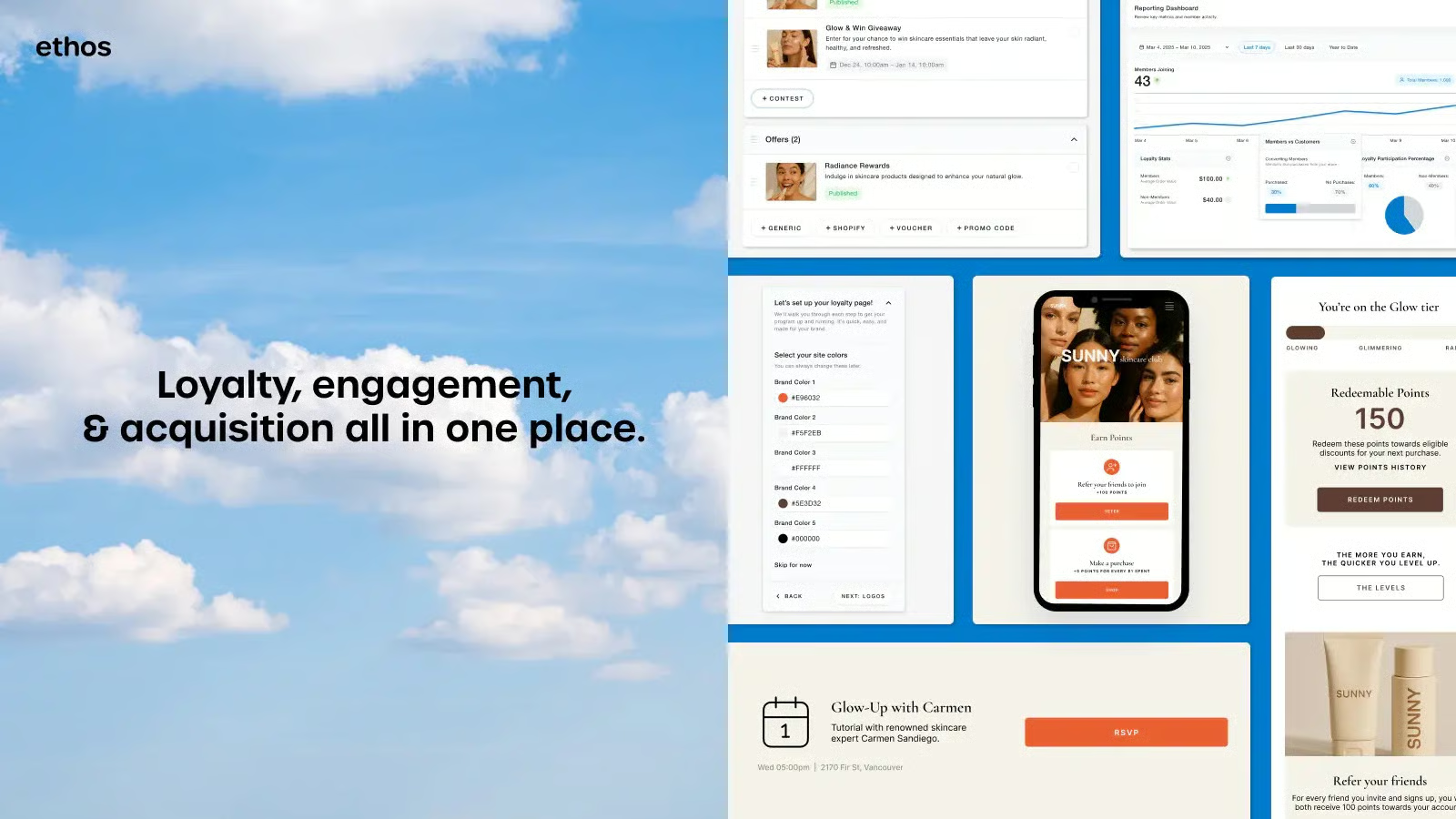

A Tool We’re Watching For the customer engagement side of the stack, we’ve seen a lot of brands switching to ethos to cut bloat. It’s a solid way to consolidate your loyalty, referrals, giveaways, and surveys into a single platform (and cut 3-4 other monthly bills in the process).

Check your stack. If you’re paying for 7 different apps to talk to the same customer, you’re doing it wrong.